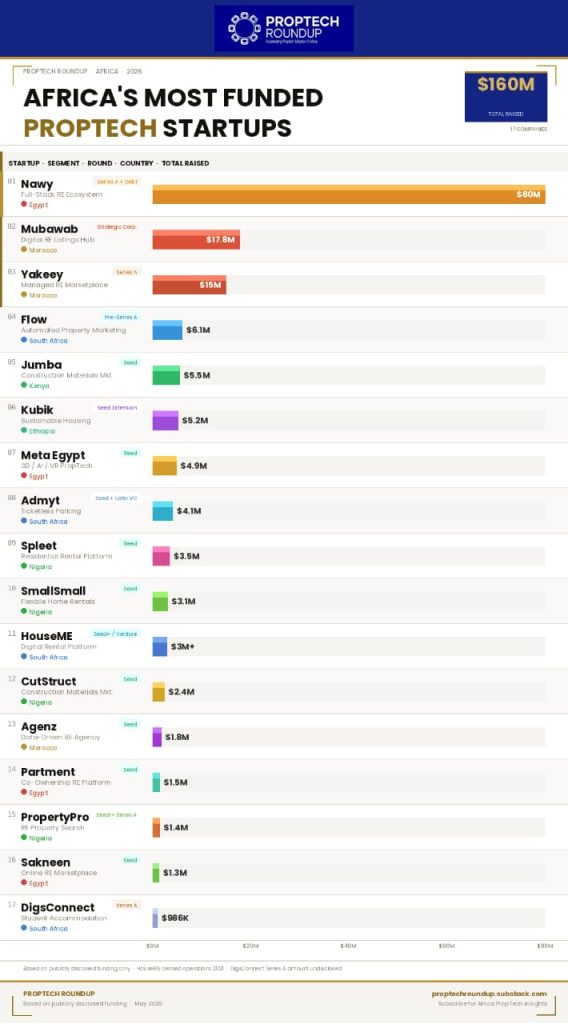

Africa’s proptech sector has attracted an estimated $160 million in disclosed funding across the most funded startups, but the distribution of that capital is uneven. The data shows a clear pattern: funding is concentrated in a small group of companies operating at the intersection of real estate marketplaces, transaction infrastructure, and construction technology rather than evenly spread across the sector.

A dominant share of capital flows into end-to-end real estate platforms and marketplaces. Companies like Nawy, Mubawab, and Yakeey reflect a clear investor preference for platforms that sit directly inside property transactions — buying, selling, financing, and ownership. These models attract larger funding rounds because they sit closer to monetisation and handle higher-value transactions compared to peripheral services.

The second visible cluster is construction and supply chain technology (ConTech). Startups like Jumba and CutStruct show that investors are backing infrastructure-related efficiency plays in real estate development rather than consumer-facing property apps. This suggests capital is also targeting bottlenecks in building, procurement, and housing delivery, not just property listings.

A third category absorbing funding is rental and flexible living infrastructure, including platforms like Spleet, SmallSmall, and similar models across markets. These startups focus on solving payment flexibility, tenant access, and rental management challenges — areas where housing affordability and liquidity constraints create strong demand for structured solutions.

Geographically, funding is also heavily concentrated. North Africa (especially Egypt and Morocco) and South Africa appear repeatedly as leading hubs, alongside a smaller but consistent presence from Nigeria. This reflects a broader ecosystem reality: proptech funding follows established real estate markets, stronger regulatory frameworks, and more mature financial systems rather than being evenly distributed across the continent.

What this reveals is that African proptech funding is not driven by novelty or early-stage experimentation. It is driven by transaction control points in real estate and construction value chains — where technology can reduce friction, improve liquidity, or unlock financing pathways in a traditionally inefficient sector.

The key question going forward is whether capital will continue concentrating around high-value real estate infrastructure platforms, or whether new funding will begin shifting toward earlier-stage housing innovation, affordability systems, and deeper supply-side solutions in African cities.

Leave a Reply