Nigeria’s latest GDP figures don’t signal a sudden economic transformation — they confirm something more familiar: the economy is still being carried by services, especially trade and real estate, while tech remains influential in conversation but smaller in measurable output.

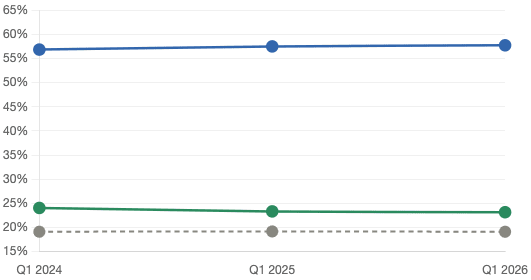

According to the National Bureau of Statistics, Nigeria’s economy grew by 3.89% year-on-year in Q1 2026, with the services sector contributing about 57.7% of total GDP. That alone is not new. What matters is what sits inside that “services” label — and it is less Silicon Valley-style tech and more traditional economic activity: buying, selling, renting, logistics, finance, and informal services that keep everyday commerce moving.

To understand this structure, it helps to zoom out. Nigeria has spent decades gradually reducing its reliance on oil, which now contributes a small share of output compared to non-oil sectors. But the gap oil left behind was not filled by manufacturing at scale or a rapid industrial base expansion. Instead, it was filled by services that scale quickly in a large population economy: retail trade, transport, real estate, telecommunications, and financial services.

Within the latest breakdown, the services sector remains the largest contributor, followed by agriculture and industry, with industry still lagging behind in structural weight. Even within services, the dominant drivers are not new economy tech startups in the narrow sense, but older and more embedded systems — markets, distribution chains, property development, mobile money-adjacent financial services, telecom infrastructure, and urban commerce networks.

Real estate, in particular, continues to act as both an economic engine and a store of value. In cities like Lagos, Abuja, and Port Harcourt, population growth and housing demand keep property development active, even when broader income growth is uneven. Trade is even more central — it is the backbone of Nigeria’s informal and semi-formal economy, linking importers, wholesalers, retailers, and millions of micro-businesses who operate outside formal industrial systems.

Tech, meanwhile, sits inside this ecosystem rather than replacing it. Digital platforms, fintech services, and telecoms are expanding quickly, but their footprint is often embedded within trade and services rather than standing as a standalone industrial pillar. That’s why Nigeria can have a visible and vibrant tech ecosystem while still seeing modest direct tech weight in GDP composition.

The broader implication is that Nigeria’s “diversification” is real, but uneven. Oil’s dominance has reduced significantly, and that alone is a structural shift. However, the replacement sectors are not necessarily high-productivity industries; they are demand-driven services that scale with population, urbanisation, and consumption patterns rather than industrial output or deep manufacturing capacity.

That leaves the economy in a familiar position: active, expanding, and increasingly non-oil — but still heavily dependent on commerce and property cycles. The next question is whether growth will continue to concentrate in these flexible but low-margin sectors, or whether industry and productivity-driven tech will eventually move from the margins into the centre of Nigeria’s economic structure.

Leave a Reply